« Reading List: Civil War Two | Main | Reading List: Public Loneliness »

Sunday, September 15, 2019

Gnome-o-gram: “Take my money. Please—I'll pay you!”

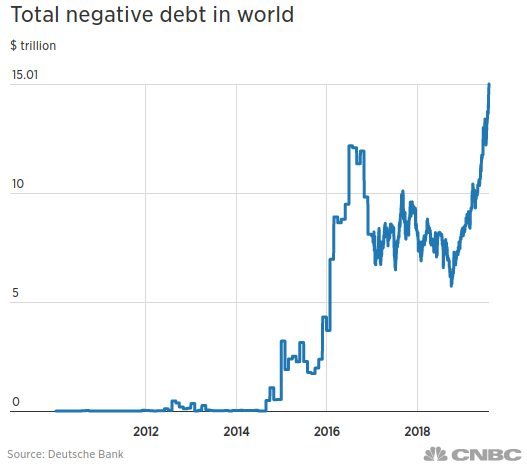

Here’s just about the craziest financial chart I’ve seen in some time.

Courtesy of Deutsche Bank, via CNBC, this is a plot of the total face value of government bonds (not, as the chart is mis-labeled, all debt) which now trade at negative yields. In other words, if you buy the bond today at its market price, hold it to maturity, and add all of the interest it will pay from now until it matures, you’ll end up with less than the price you paid for the bond. And this is in “nominal currency”, not accounting for any depreciation in the purchasing power of the money you get back (due to inflation) compared to what you paid for the bond.

Fixed-income investing (bonds, time deposits, etc.) used to be easy to understand and, let’s face it, boring. It’s supposed to be boring: “gentlemen prefer bonds” because assuming the issuer doesn’t go bust and default on the debt (which can’t happen with bonds issued by a government that can print its own money—the money you get back may be worth less or worthless, but you’ll get it back for sure), you’ll earn the steady rate of income quoted for the bond when you bought it all the way until maturity, when you get your money back. As interest rates go up and down, the market value of the bond will fluctuate, but that doesn’t matter if you hold it until maturity, when it pays off at face value.

Usually, the longer the term of the bond, the higher the rate of interest you’ll earn, since investors demand a greater yield in return for tying up their money for a longer period of time. This isn’t always the case: in fact, we’re presently in a period of an inverted yield curve, which I discussed here in an earlier gnome-o-gram.

But what could possess investors to bet on a sure loser: an investment which is guaranteed to pay back less money than was paid for it? And this isn’t just some rubes who fell for a fast-talking salesman: there are fifteen trillion US dollars worth of these bonds in the portfolios of institutions (banks, pension funds, insurance companies, corporate treasuries, government agencies) worldwide.

The reason is basically fear (and, in the case of some institutions, mandates that they hold some fraction of their assets in government securities). With yields on even substantially risky bonds in the cellar, at least you don’t run any risk with the government bond and you only lose a little money. (For some reason, the alternative of simply ordering up a pallet of high-denomination bills from the central bank and putting them in the vault doesn’t seem to occur to these people, or is considered beneath their dignity.) And with equity markets looking over-extended and volatile, that option is increasingly unattractive.

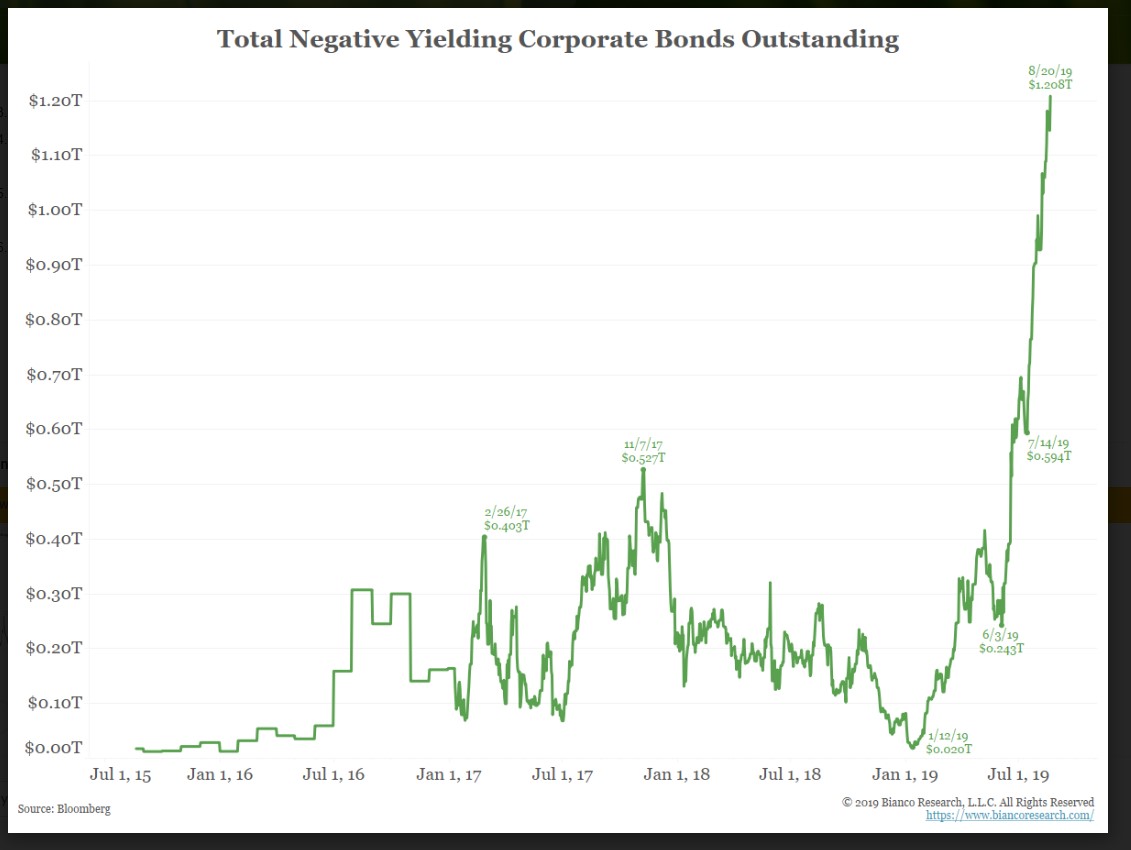

It isn’t just government bonds, either. Here’s a chart by Bianco Research, published by Market Watch, showing negative yielding corporate bonds in the hands of investors exploding from zero to US$ 1.2 trillion in the first eight months of this year.

When a recession occurs, the principal tool in the hands of a central bank to promote recovery is lowering interest rates. But conventional wisdom among analysts used to be that when rates were already close to zero, there “weren’t any arrows left in the quiver” because “rates can’t go negative”. Well, it appears they can, because they have.

Now, I guess the question is how far into negative territory they can go. If a recession sets in over the next year, I suppose we’ll see.

Posted at September 15, 2019 14:07